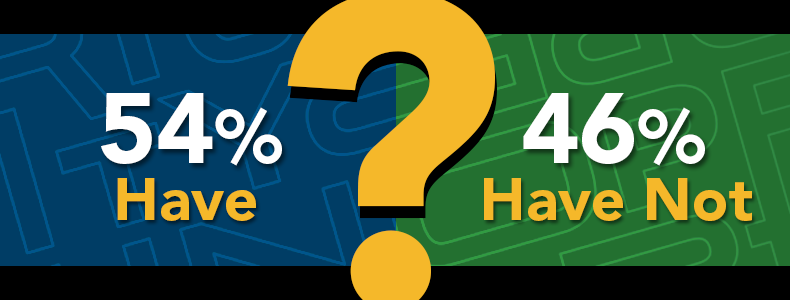

Life insurance is considered an essential part of a long-term financial plan. Two-thirds of Americans say they recognize the need for life insurance but many do not have adequate coverage to protect their families1. Yet, only 54 percent of Americans say they own life insurance in 2020.2

Why is that? A general lack of knowledge may be a factor in why people procrastinate, don’t feel the need to buy life insurance, or have insufficient coverage for the needs of their situation.

What is life insurance?

Life insurance is a contract you make with an insurance company in which you agree to pay premiums to the insurance company. In return, the insurance company agrees that upon your death, they will pay the amount you chose as the death benefit to the person you designated (if benefit is payable according to the terms of your policy) as your beneficiary. Life insurance is a financial product designed to help protect loved ones from the financial uncertainty that may occur when you are no longer there.

A study by the Pew Research Center asked people what gives the most meaning, fulfillment, and satisfaction — 69 percent said family.3 Don’t we all want to protect what means the most to us?

Common Fears and Misconceptions about Life Insurance

That’s morbid!

Facing your own mortality and actually talking about it can be difficult, but it’s a conversation that needs to be had. Denial is not your friend, and here’s why: your age is one factor that helps determine your life insurance premiums. Unless you have found a way to age in reverse, time is marching on, and the longer you wait, the more expensive life insurance will become for you.I’m perfectly healthy. I don’t need it.

In addition to your age, the other factor with the greatest effect on the cost of life insurance is the state of your health. Perfect health today is no guarantee for what it will be in the future. If your health does take a downward turn, you may find life insurance is expensive, or you may not be able to qualify. Besides, life insurance is for the living, the loved ones who depend on you and could face financial adversity when you die.I just don’t think I need it yet.

When you’re young and single, you may see life insurance as a need you’ll face at some point in the future; maybe after marriage, or the birth or adoption of a child. These important life events help make us more aware of the importance of life insurance to meet the four most common needs a family typically faces upon the death of an income earner: final expenses, income replacement, mortgage, and education. Just because you’re single, however, doesn’t mean you are exempt from the need for life insurance. Do you have student debt? Do you have credit card debt, a car loan? Do you own a home? Did someone else co-sign any of those loans? Most debts do not just go away when you die, and your loved ones may be responsible for them.I can’t afford that; life insurance is expensive!

Most people estimate life insurance costs three times more than it actually does.1 Remember, the two biggest factors that determine the cost of life insurance are your age and your health. Clearly, there is no better time than now to buy life insurance.

Where’s the disconnect?

For many, the disconnect may be at the point when they try to discern which kind of life insurance they should buy. There are two main types — whole life and term life — but there are variations within each to make them suitable for meeting a variety of needs and circumstances. It’s one thing to research life insurance products on the internet, but it’s another altogether to purchase this important protection for your family with the confidence you have chosen the right policy(ies) to fulfill your family’s needs.

Enter the licensed insurance agent

We understand the desire to do online research so you aren’t jumping blindly into purchasing life insurance, but when you are ready to sign on the dotted line, we recommend contacting a licensed insurance agent to guide you. This is why we say life insurance is ‘sold’ rather than bought.

Insurance agents must be licensed by the state(s) in which they sell and for the specific insurance product(s) they sell. The biggest reason state governments regulate the insurance industry is to protect American consumers,4 which can make the prospect of buying life insurance much more comfortable.

A licensed professional life insurance agent can:

- Do a personal assessment of your family’s needs and financial goals

- Help you navigate the choices for your family

- Help you anticipate your family’s changing needs at different stages in life

- Address any misinformation or concerns you may have about life insurance

- Help you fit the life insurance coverage you need with your budget

There are many reasons buying life insurance may not be on people’s priority list. A licensed insurance agent can explain the need and help you choose appropriate coverage for your needs and budget with confidence.

- Life Happens, 2019 Insurance Barometer Study: Nearly Half of Americans More Likely to Buy Simplified Underwritten Life Insurance , (August 25, 2020)

- Statista, Distribution of life insurance ownership in the United States in 2020 (August 25, 2020)

- Pew Research Center, Americans Find Meaning in Life, (August 26, 2020)

- NAIC, State Insurance Regulation, (August 27, 2020)

Categories: Insights for Sales Professionals, Careers in Insurance, Insurance Agents